The aftermath of an accident can be highly frustrating, especially when your vehicle sustains damage. It can worsen if the insurer deems your car a total loss and offers a low settlement amount. What can you do in this scenario? Would you consider accepting the settlement or walking away in frustration? Wrong! There is a third solution; you can seek assistance from Gig Harbor, Washington, total loss appraisal clause experts.

At ADR Claims, we are a team of total loss appraisal clause experts. It doesn’t matter whether you don’t know anything about total loss or just need guidance; we are here to help you throughout the process. We will help at every step so you get a fair settlement for your car.

What is a Totaled Vehicle?

When a car is involved in an accident, and its estimated repair value meets or exceeds the total loss threshold limit, the insurance adjuster declares it a total loss. This is also known as a car being totaled. A total loss threshold is the percentage of a vehicle’s value that determines whether it is a total loss. As per regulations set by governments, the total loss threshold by state varies.

Learning About Total Loss Appraisal and the Clause

Many insurance companies give the policyholder the right to call for an appraisal under their policy. This is known as a total loss appraisal clause. If the insurance adjuster offers a lower settlement amount, you can invoke the appraisal clause and have your vehicle assessed. They provide you with a market-based, comprehensive appraisal report to show to the insurance company and request a fair settlement.

What Car Owners Get in an Appraisal?

If you use the total loss appraisal clause included in the insurance policy, you will likely get the following things from the auto appraiser.

- A licensed and comprehensive appraisal report, containing market data, listings, and comps to precisely represent your vehicle’s total loss value.

- Continued assistance and guidance throughout the insurance claim filing settlement process from your selected Gig Harbor, Washington, total loss appraisal clause experts.

- A full representation during the appraiser-to-appraiser discussion.

When to Have a Total Loss Appraisal?

Whether you are seeking a total loss appraisal in Arizona, Washington, or another place, there are a couple of things you must take into consideration first. You need to decide whether invoking the appraisal clause is worth it. The points mentioned below can help you make that decision.

- The insurance company deems your vehicle a total loss, and you are confident that the settlement amount they offered is lower than what you deserve.

- You have tried negotiating with the insurers, but that was of no use, and only a certified appraisal report can help you now.

- You are prepared to tackle the exhausting settlement process after you invoke the appraisal clause.

- You need the maximum amount to change your current car.

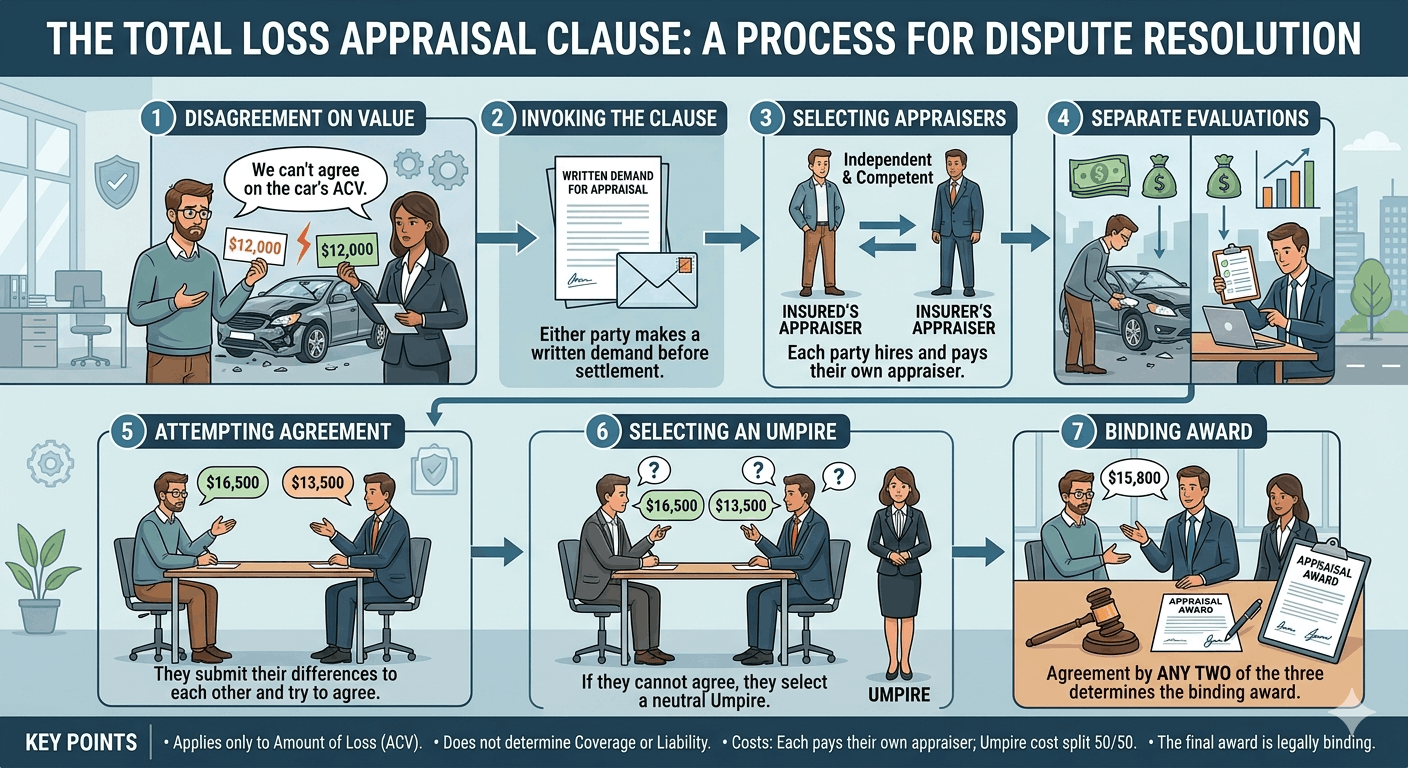

Total Loss Appraisal Process: Step-By-Step

The total loss appraisal is a complex process that feels exhausting and confusing at times. We intend to help you, so we explain the process into five simple steps.

Invoking the Appraisal Clause

The process begins with you sending a formal written letter to the insurance company informing them that you are now invoking the appraisal clause, as you were not able to reach a mutual settlement amount. You can also email the insurance company, but they may overlook it, so a written letter would be best.

Selecting a Certified Appraiser

You and the insurance company hire a certified appraiser and compensate them for assessing the total loss amount of your damaged car. Make sure that your appraiser is neutral and isn’t connected to the insurance firm.

The Appraisal Process

Both appraisers carefully assess the loss of your vehicle and discuss their findings. Then, they try to reach a mutually agreeable settlement amount.

Calling for an Umpire

If the two appraisers are unable to determine a mutually agreeable claim settlement amount, they select a third-party, neutral appraiser, known as an umpire. The umpire checks the positions and documentation of the two primary auto appraisers. When you call the umpire, both you and the insurance company must cover half of the umpire’s hiring cost. The amount two of the three appraisers agree upon is a binding decision.

Settling the Claim

At last, you submit the written appraisal award to the insurance company. Then, the insurance company pays you the amount agreed to in the appraisal process.

We are My Creative Web, a professional appraisal firm serving car owners for a long time. If you are looking for Gig Harbor, Washington, total loss appraisal clause experts, we have a team of them dedicated to helping you in the settlement process. We can also help you with a diminished value claim in California if you are filing one. Contact us right away and book your auto total loss appraisal service.